Are Home Improvement Stocks Now Undervalued?

[ad_1]

The lockdowns of 2020 may perhaps have prompted buyers to set extra money towards their surroundings, boosting profits for dwelling improvement stores Lowe’s (NYSE:Small) and House Depot (NYSE:Hd), but the economic and housing availability crunches of 2022 are retaining them there.

Furniture, electronics and dwelling business set-ups aimed at generating household a far better place to live and operate fueled 2020 paying for, but with consumers struggling with soaring costs of gas and meals, theyre heading to dwelling advancement merchants to take care of repairs them selves and start gardens. This is retaining progress at Lowe’s and Property Depot sturdy, earning them each most likely financially rewarding portfolio additions this summer months, in my viewpoint.

Both choices have growing dividend yields, producing them attractive for benefit investors hunting to make passive money as very well. Ahead of you insert either of these home improvement shares to your portfolio, though, there are some shortcomings to contemplate.

Lowes

Lowes (NYSE:Minimal) is a residence improvement retail chain operating in the U.S., Canada and Mexico. It features goods for construction, routine maintenance, repairs and transforming. The housing marketplace could be cooling a little from the highs of 2021, which might encourage jobs in the residence youre in.

Revenues for the company have doubled over the earlier 10 years, and earnings per share are expected to increase about 13%. Lowe’s has a dividend produce of 1.66%, and the company has a very long monitor record of increasing dividends. That could assistance sweeten the offer for traders.

Analysts amount Lowe’s a acquire, even although bulls feel the business faces pitfalls from growing desire charges, supply chain challenges and flattening housing costs. Its worthy of noting that the median age of houses in the U.S. is 39 several years, an age when residences will require an increasing amount of money of upkeep and could be candidates for remodeling.

Lowe’s will get a GF Rating of 96, driven mostly by leading rankings for profiability and expansion.

Property Depot

Surpassing forecasts in nine of the previous 10 quarters, another significant U.S. property improvement retailer, Property Depot (NYSE:High definition), not long ago reported 10.7% expansion in net product sales calendar year-over-calendar year.

Home Depot counts professional contractors between its biggest shoppers, and their large-ticket purchases ended up up 18% in the course of the past calendar year. EPS has developed 17% more than the past a few several years and profits is up 8% above the past calendar year, getting it a get rating from analysts.

House Depot has a dividend yield of 2.26%, making it the far more desirable of these two stocks for those people in research of dividends.

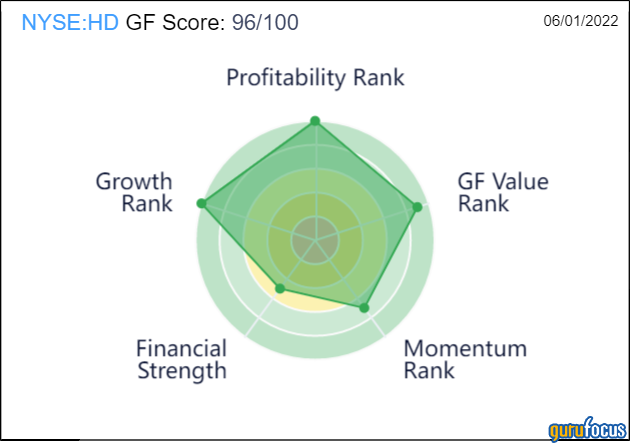

Like Lowe’s, House Depot also has a GF Rating of of 96/100. In addition to superior advancement and profitability, it scores better than Lowe’s for GF Worth, though it loses details for weaker momentum.

This posting first appeared on GuruFocus.

[ad_2]

Source link